Cry Panic! And Binge-Watch Industry

In the fall of 2008 as the Great Financial Crisis unfolded, I felt flashes of panic. The photograph below, Desperate Man, was prominent on our bedroom wall and every time I looked at it, I’d feel like seizing my own hair.

Lehman had failed, the stock market was on its way to a 50% crash, and the Bernie Madoff fraud had been revealed. Although I was not a Madoff victim, the scale of his fraud––headline of $50 billion–– combined with the failures of Lehman and other institutions rocked my confidence.

Perhaps the narrative I’d been telling myself about the financial world was completely divorced from reality. Perhaps I’d been clueless about the true nature of Wall Street and how it all worked. I wondered how it was possible to know the true value of anything I owned. Or whether in fact I could really be certain that I owned what I thought I owned.

I was 46 years-old and senior enough to have earned a fair amount of responsibility as an investment manager. For the investments in my portfolio, it would be mostly my burden to decide which investments to save and which to let perish.

My emotional response was to take flight, to flee this financial world that had suddenly become hostile, cruel, unrecognizable. Flee from my responsibilities that had turned from a source of pride to a source of self-doubt and shame. I hated losing money for my partners and investors.

I could cash out and pick up the pieces. Find a career less stressful.

I told my wife Debbie how scared I was. Soon thereafter, at a December black-tie benefit at Chelsea Piers––benefits sailed on through the gloom––Debbie asked an older, wiser, and very good family friend to chat with me. He told me to be patient, that there’d be good opportunities that came out of the downturn for me and for my positions. I listened to him and he was right.

“Narrative is all that matters”

I’ve recently binge-watched the TV show Industry about a group of young finance and business professionals who make and lose fortunes, are beautiful and fit, snort enough cocaine to kill a small horse, and have frequent and explicitly staged sex with one another in fabulous locations. 1

The show is excellent and not in a “I read Playboy for the articles” way. It’s well acted and well written, and consistently clever. Its breakout star is Marisa Abela as Yasmin, the rich girl with a tortured past.

More than anything, however, Industry captures the zeitgeist of our times––the predominance of narrative over reality.

The creators have scripted much of the show’s financial shenanigans in a brazenly inaccurate way. Many of the numbers, timeframes, and legal proceedings don’t make sense. But it doesn’t really matter. The details are subsumed beneath the dramatic power of the narrative and the appeal of the complex characters who come with a mix of flaws and virtues.

The creators are ex-finance pros so maybe they created cartoon scenarios on purpose to underscore the often-spoken motto of the show: “narrative is all that matters.”

Casinos vs. frauds

Industry’s creators get away with their version of finance theatrics (even with a pedantic stickler like me) because the schemes they write about are generally on the right track in portraying our hyper-gamified, casino economy where value is what someone says it is on any given day.

Naturally, there are financial frauds on the show. That’s inevitable; there’s always been frauds in fiction and in real life.

The financial frauds that Industry showcases are realistic. Madoff happened because investors wanted desperately to believe his mathematically improbable returns were true (akin statistically to filling out a perfect NCAA bracket!). 2

Investors are no match for fraudsters who regularly trick accountants and regulators to bless their financial statements. As Eric (my favorite Industry character) said recently on fictional CNN,

“You want me to give you a list of the number of times regulators have been wrong. How long is your show?”

The narrative, on the other hand, is different than fraud. It does not hide. It’s all out in the open.

That six-million-dollar banana

All the real-life buyer got is a sheet that instructs you how to tape a banana to a wall, because the banana is real and will soon spoil. The sheet is first sold for hundreds of thousands of dollars and then for over six million dollars. It’s not a fraud. The buyers know exactly what they’re getting.

The narrative behind the banana instruction is that if someone made a fortune buying it for a few hundred thousand, why can’t the six-million-dollar buyer make a fortune off the next buyer who might pay $60 million? One number is just as untethered to reality as another. If Bitcoin can trade at $100,000 a coin, why can’t it trade at a million dollars?

On Polymarket, a prediction site, you can bet on whether Bitcoin will go up or down in the next five minutes. On Industry, time is super-compressed. Fortunes and reputations go up and down in minutes or seconds.

One of the trader characters, Rishi, is a compulsive gambler. When he keeps betting red on roulette and keeps losing, we watch him watching the wheel spin and the ball bounce, and we understand it’s a perfectly accurate extension of how Industry presents his day job. And financial markets today.

Perpetual assets

Every asset---Rishi’s casino chips, the sheet of paper that instructs you how to mount a banana on your wall, every crypto coin, every share of stock, every parcel of real property---must be owned by someone. Barring a few exceptions, that truism does not change. The assets I’ve mentioned can be bought and sold but unlike debt there is no one obliged to redeem them from you for any specified or certain value at any certain time. 3

They are perpetual assets traded among ourselves in a closed loop, a merry-go-round, at prices set by human buyers and sellers based on the current narrative. That they can often be sold at relatively consistent prices over the short term is a human construct that’s usually true but not guaranteed.

Imagine a world where after you bought a perpetual asset you could never sell it. How would you value it?

If it’s an asset that doesn’t produce any utility or cash flow to you––a piece of art, whether a banana or a Rembrandt on the wall––you’d value it for the aesthetic pleasure it gave you. If it were a financial asset, like a share of stock, the only rational way to value it would be for the present value of future cash flows.

What I’ve described is the reality of our world when viewed as a whole. And when the narrative spins away from this hard truth, the reality can bite. As Bethany Mclean, a great financial journalist, recently writes:

“When no one can find an anchor for the fundamental value of companies, the market starts searching for a narrative.” 4

If the bubble is pricked

It would not surprise me if the U.S. stock market declined 50% as it did from the 2000 and 2008 peaks. In that scenario, more speculative assets like banana art and crypto would likely suffer worse fates.

That said, I’m not betting on that happening and I make no claim to any special perspective or predictive power. Admittedly, it’s hard to imagine the stock market getting cut in half after 17 years of stocks rising, But the numbers and the history I look at suggest it’s a risk to take into account.

One might say, so what? Each share of stock is still held by someone. All that’s happened is that investors collectively decided on new, lower values for the same assets they collectively hold.

Plus, the stock market has always come back.

And for young investors who have not yet or are just starting to invest, a 50% decline can be seen as a great opportunity. Now they get to buy the same assets at a 50% off sale.

All this is true but it ignores human emotion and how the financial economy can affect the real economy. Because when people feel wealthier, they spend more. When people feel less wealthy, they spend less.

Tightening our belts at Big Pink

In December 2008, we were at the Big Pink diner in Miami when I spoke to our three children, (ages 20, 18, and 15) about the financial crisis and the Bernie Madoff fraud. 5

I told them our net worth had declined substantially. I was uncertain what would happen to our income and our wealth going forward. “Mom and I are planning to tighten our belts.”

Until things recovered, we reduced our spending where we could. 6

This is called the wealth effect. The popping of a bubble will make many families reduce their spending.

When many families react in similar fashion, the reduced spending reverberates across the economy. Although the wealthy may lose the most in dollars, the decline in spending hits hardest those with the greatest amount of precarity. It also impinges upon philanthropy at the very time it’s needed most.

The state we’re in

The wealth effect of a bubble deflating in 2026 or 2027 could be more severe than it was in 2000 or 2008. A few facts to consider:

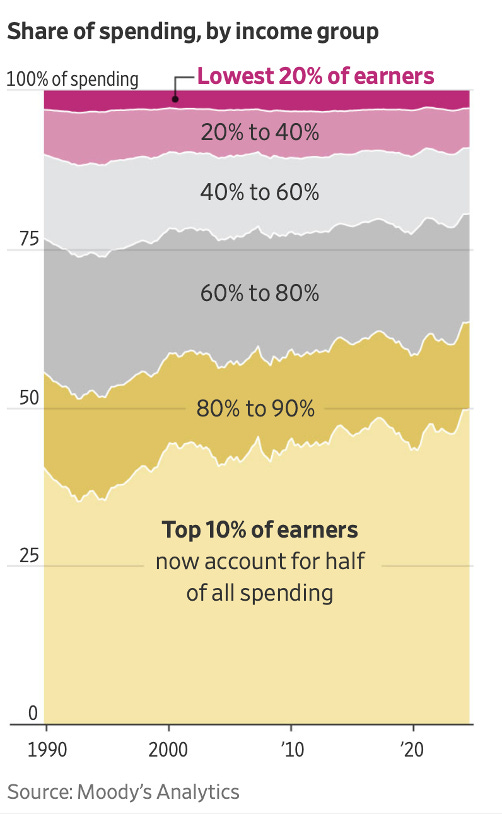

1) Wealth is more concentrated at the top and so is spending. The top 10% are responsible for about 50% of all consumer spending. 7

2) The amount of wealth represented by the stock market has increased significantly. It’s estimated that the stock market is worth about $70 trillion today vs. $18 trillion at the 2000 peak and $20 trillion at the 2008 peak. As a % of GDP, it’s never been higher in post-war history and perhaps ever. That wealth is concentrated among the wealthiest, the big spenders.8

3) Federal debt is now 120% of GDP vs. 60% in both 1999 and 2007 (the years prior to the 2000 and 2008 crashes). In 2008, the government was able to function more or less cohesively to address the financial crisis. Today the government has little fiscal room to address a crisis without risking a debt crisis and scant unity of rational purpose. 9

So, our country is particularly fragile right now to the risk of a downturn caused by a change in the narrative of what we collectively decide our assets are worth.

No one should root for a downturn. Good luck to us all.

Question for the comments: Is a potential asset value bust something you worry about, and either yes or no, why?

“Enough cocaine to kill a small horse” is a line from the movie Good Will Hunting

A call back to last week’s post that featured a. natasha joukovsky’s book Medium Rare and the road to a perfect NCAA tournament bracket.

Exceptions are when a corporation goes bankrupt, is acquired, or repurchases and retires its own shares. For physical assets, the exceptions are destruction either through peril or decay.

From an article in The Free Press on 2/26/26

I remember having tise talk; thanks to my daughter Lauren for remembering the specific place.

I recognize it would be ludicrous to call our spending reduction a sacrifice, hardship, or even an inconvenience.

Total Stock market Capitalization, FRED data

FRED data

Someone asked me what’s the scariest movie I’ve ever seen and I said “The Big Short”. You had to live it.

Are you aware of the cliffhanger created by the opening lines of today's post?

"The photograph below, Desperate Man, was prominent on our bedroom wall and every time I looked at it, I’d feel like seizing my own hair."

When and why did this upsetting artwork end up in your bedroom? When and why did you decide to take it down? Did Debbie play her usual salutary role in this decision?

Also, because of my long-ago art school background, it's technically a print rather than a photograph.