A Man Who Dies Rich Dies In Disgrace

So said Andrew Carnegie, 19th century steel magnate extraordinaire, who gave away almost his entire fortune.

Over the past few years, my wife Debbie and I have increased the time and resources we devote to not-for-profit organizations that help people who have urgent material needs.

My motivations for giving are complex.

I have family role models of community involvement going back generations with my mother Jill Roberts and a paternal great-grandfather Sam Rottenberg standing out. They would be proud of what we’re doing, which makes me happy.

When I’m engaged in philanthropy, I feel most deeply connected to my Jewish identity. I’m far more motivated to fulfill the commandments of ethical acts––doing our part to “repair the world”––rather than to observe the commandments of prayer, faith, and ritual. 1

Ideally, I would embrace both the ethical and the spiritual aspects but that’s not how I’m constituted.

Giving makes me feel good because it gives me agency to change lives for the better. I can read the news and curse the darkness––and I often do––but I can also light candles that make the darkness a little less dark.

All that said, my wife and I are not saints. We’re very far from renouncing worldly goods and material comforts and pleasures. Our spending on ourselves and our family creates limits to our giving, which I discuss below.

This Monday at 4 pm EST, I will be interviewed by Jeremy Ney about my approach to philanthropy and related topics. Jeremy writes the Substack American Inequality, which is a tremendous source of information on the topic and a pleasure to read if the substance doesn’t make you too angry.

The invitation to our Live! interview is here.

The breach

America’s wealth has never been greater while inequality has never been greater. At the same time, our social safety net is being weakened in exchange for lower taxes and record national debt.

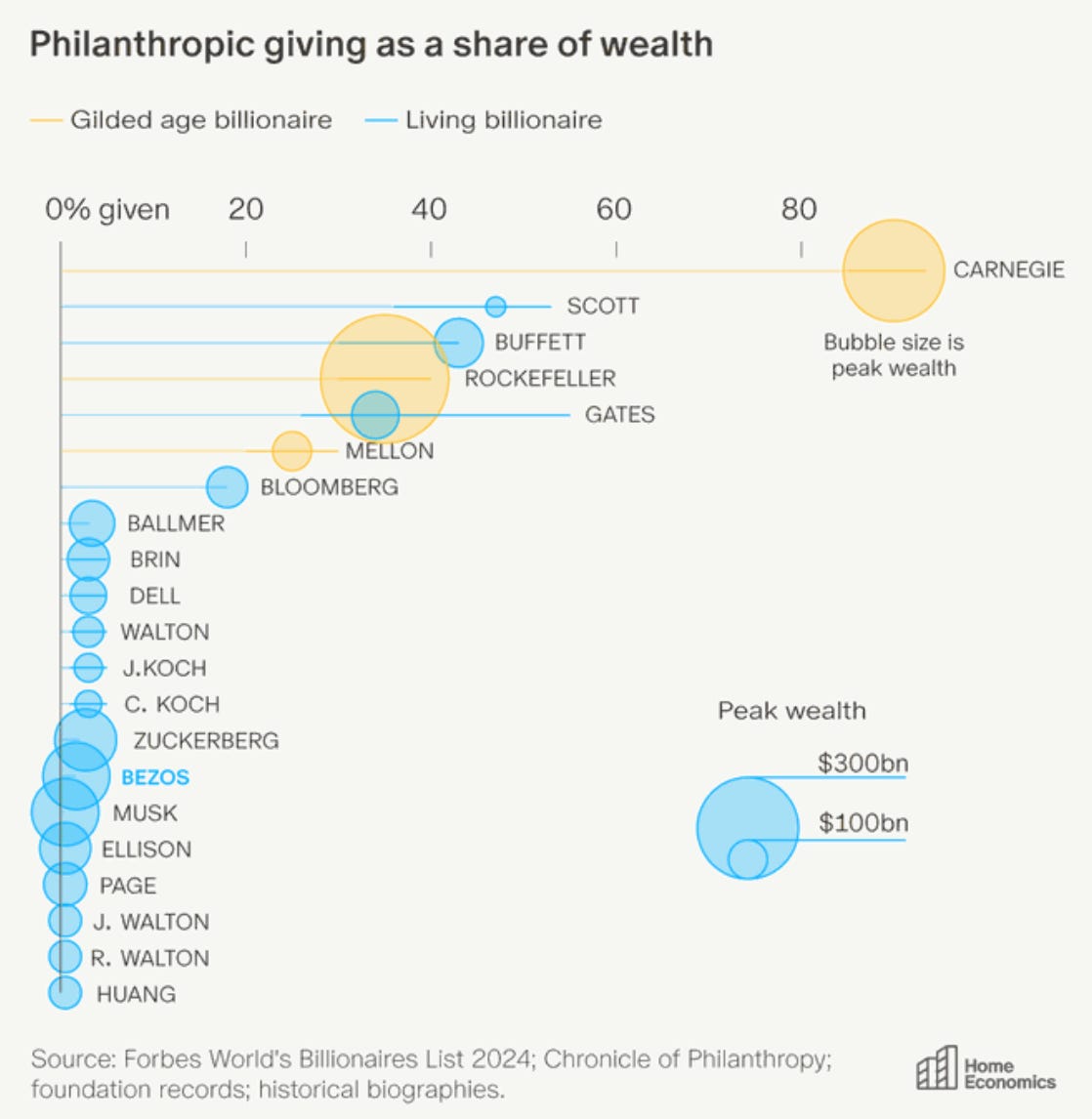

Philanthropy has not stepped into this breach. Jeremy Ney’s latest article Why Philanthropy Is Silent In The Golden Age Of Wealth contains the fascinating chart below comparing the giving of the big three plutocrats of the first Gilded Age––Carnegie, Rockefeller, and Mellon––with the giving of our current crop of plutocrats.

I wrote about Carnegie’s Gospel of Wealth a few years ago. My post was titled Would Andrew Carnegie Have Flown Economy, linked in the footnote below. 2

On the scale of this chart, I would be an imperceptible blue dot, somewhere beneath Bloomberg’s bubble, planning to march my little dot eastward past Mellon’s bubble.

My calculations

For every two and a half dollars we spend on ourselves and our family, we donate around a dollar. That ratio came about organically rather than as some grand plan. Over time we’ve added not-for-profit organizations to our portfolio of giving. And our spending has also increased.

Every week I keep track of our spending and keep track of our financial assets. I’m a spreadsheet guy.

I keep a long-term projection of what happens to our financial assets given an assumed rate of after-tax investment return and an assumed inflation of both our spending and our giving.

There’s an infinite number of “what if” games to play but my base case, meant to be conservative, although far from a disaster, is a 4% after tax rate of investment return and a 2.5% inflation rate. With those assumptions, after thirty years, at the age of 94, we still have some financial assets left, although greatly diminished in real, inflation adjusted, terms.

That makes me comfortable with our current rate of giving and increasing it with inflation.

The calculation for billionaires is far different. Their spending is likely to be a rounding error.

But for the less exceptionally wealthy––and there are far more of us––I think my methodology is useful. As long as you realize that a spreadsheet is a tool you control and not the other way around.

Solutions

In our upcoming interview, Jeremy Ney will ask me about solutions to address the insufficiency of philanthropy to make up for the gaps in our social safety net.

There are a few straightforward changes to the tax code that can indirectly tax wealth and encourage more charitable giving. They both have to do with capital gains taxes. I think direct wealth taxes are a poor way of addressing inequality as I discussed in a prior post. 3

Currently, long term capital gains (long term defined as a year and a day of holding period) and most dividends are taxed at a maximum federal rate of 20% vs. a maximum rate of 37% for ordinary income, including wages. As well, when someone dies, all their assets are “stepped up” for tax purposes to the asset values at death so that all the unrealized value up to that point in time remains forever untaxed. 4

I suggest that both of these provisions be changed so that all income, including capital gains, be taxed at ordinary rates and the step-up at death be eliminated and the estate be required to pay the capital gains tax.

These changes would increase the taxes paid by the holders of wealth. The changes would also discourage the strategy of “spend, borrow, die” wherein a wealthy holder borrows against their assets to support their spending and avoids paying gains taxes when they die and their assets are “stepped up.” 5

From a philanthropy point of view, I believe these changes would incentivize more giving of appreciated assets since there would otherwise be no escaping eventual taxes on gains.

Of course, the more charitable giving there is, the less paid in taxes since charitable giving creates a tax deduction.6 But if the gap we’re solving for is between government tax revenues and philanthropy, then more giving is not a bad thing.

Objections to my solutions

One objection is that the wealthy might “park” their assets in foundations and donor advised funds where most of the assets could grow without being given away. But the rate of giving (donations as a % of assets) from donor advised funds is above 20%. Foundations must give away 5% of their money annually. So eventually those assets will find their way into philanthropy. 7

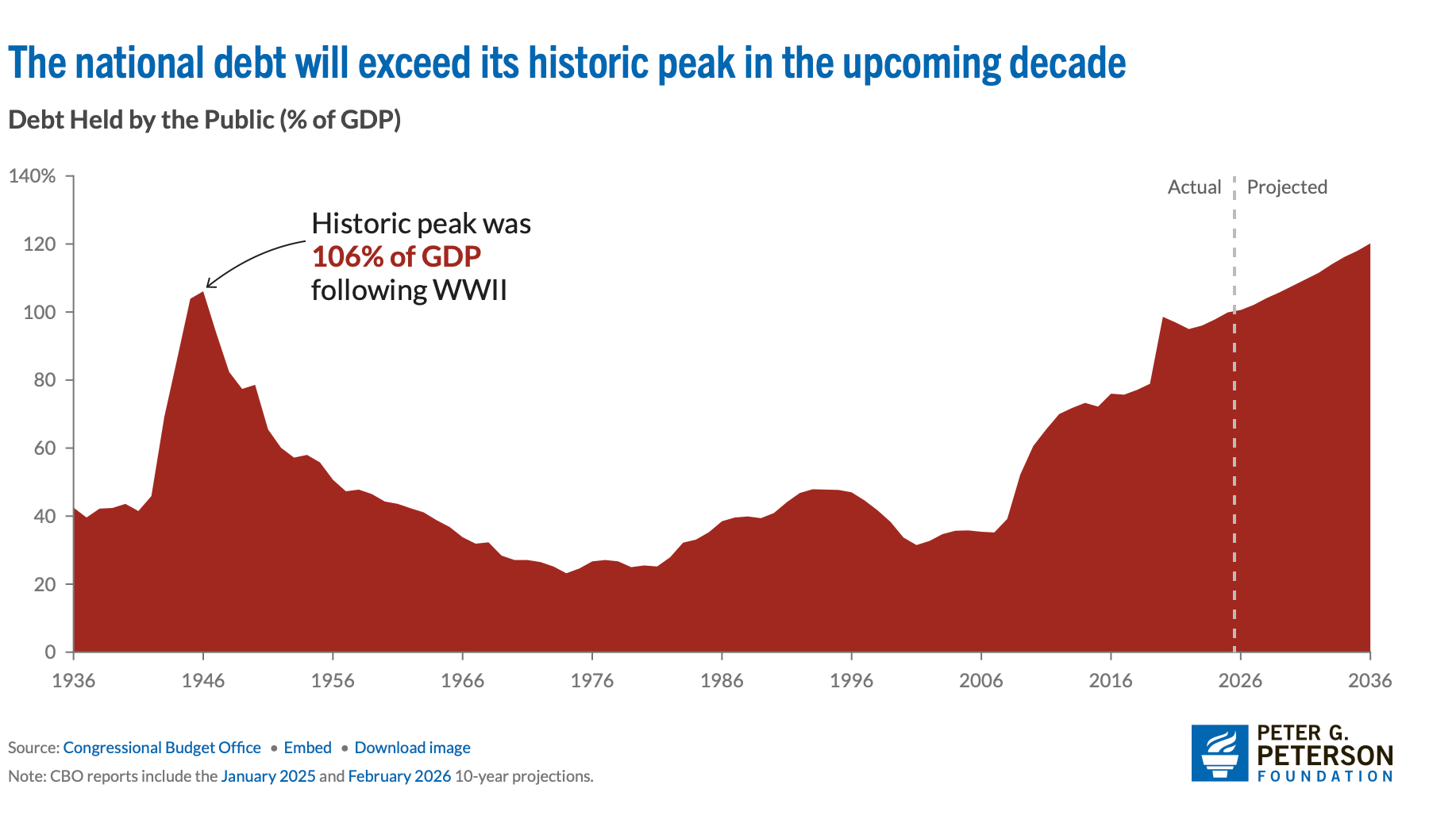

The larger objection to my solutions is that they are far too modest. To provide the federal government with enough money to keep our national debt at reasonable historical levels (see alarming chart below) and provide the government enough funding to repair the social safety net, far more tax revenue is needed.

That means higher income tax rates at brackets that reach deep down into the ranks of the wealthy and the affluent. Certainly, a higher rate than 37% at the top.

We may eventually have no choice but to radically change the tax code and introduce a national sales, or value-add, tax as nearly every other developed nation has done.

Illegal loopholes

With all the current legal loopholes available, many wealthy American taxpayers still push their luck in trying to abuse the tax code through evasion rather than avoidance.

Recently I read about one such scheme. If you become a legal resident of Puerto Rico and you sell an asset for a gain, you do not have to pay capital gains taxes on the portion of the gain that occurred while you were a legal resident of Puerto Rico. 8

But apparently the rule has been sorely abused. People who knew they were about to realize a huge gain moved to Puerto Rico shortly before realizing their gain and then claimed falsely that all of the gain was realized while they were a resident of Puerto Rico. When, on the contrary, it was evident that much of the gain took place before they left the mainland United States and so on that portion of the gain, taxes are owed.

These accused tax evaders received legal opinion letters from lawyers, now under criminal investigation, so they could claim they were just following advice, which is the same morally obtuse excuse as “just following orders.”

Question for the comments: In which ways does our current tax, social safety net, philanthropy situation bother you, if at all?

At the same time, I think as a Jew it’s important to be ritually knowledgeable and understand the rituals I do not observe. Ritual and tradition have been and will continue to be vital to maintaining Jews as both a people and a religion.

This does not include the 3.8% medicare tax on all investment income nor state and other local taxes.

The “step up” works like this. If you were lucky enough to buy a stock for $10 that increased to $100, then when you die, the stock’s tax basis will be stepped up to $100 so anyone inheriting it will not have to pay taxes on the unrealized gain of $90. That is the current law.

The so-called spend, borrow and die strategy works like this. If you founded a company like Amazon and hold stock worth $100 billion with a tax basis of zero, you could borrow against that stock to pay all your living expenses rather than sell your stock. Then when you die, your unsold stock can be sold at its current market value of $100 billion without any taxes owed and some small portion of the proceeds used to pay off the debt.

There are practical reasons why this is rarely a good strategy including the fact that when you borrow for the purpose of spending, the interest expense on that borrowing is not tax deductible. If you’re borrowing at 4% to avoid capital gains taxes, after six to seven years you’d have been better off selling and paying the capital gains tax.

Also, if you’re incredibly wealthy, why bother with borrowing anyway? In fact, Jeff Bezos sold many billions dollars of Amazon stock in 2025.

The tax deduction may be worth about 35 cents on the dollar. If you give appreciated stock, you get the 35 cents benefit plus avoiding another 24 cents of capital gains. However, you are still making a net contribution of about 40 cents on the dollar so it’s a myth that charitable giving can make taxes disappear without any financial contribution from the donor.

Donor advised funds (DAFs) are themselves 501c3s that allow donors to make donations to a DAF and then use those donations to direct charitable contributions over time. I’ve found that using a donor advised fund has encouraged me to build up resources in our DAF earmarked for giving. I do not view DAFs as a loophole or abusive.

NYT article, 4/30/26. An excerpt;

“According to the letters from Senator Wyden, shortly after Mr. Morehead relocated to Puerto Rico in 2021, his firm sold a large position, generating capital gains of more than $1 billion. The committee has received information from a whistle-blower who claims Mr. Morehead accrued most of his share while he lived in California, and improperly avoided over $100 million in federal taxes.

In a statement, Mr. Morehead said: ‘I acted appropriately at all times with respect to my taxes. I consulted with professional tax advisers and relied on their advice. Any claim otherwise is simply incorrect’’.”

I worry about major philanthropy as a substitute for government, since there is no democratic process for deciding where money goes. (Of course that assumes a democracy...) There's plenty of literature about where the rich donate, and anti-poverty organizations are generally lower on the list than arts organizations, educational institutions, and health-related causes.

BUT, I'm also tremendously worried about the cultural trend, a la Peter Thiel, to disparage philanthropy and limit giving. The lack of trust in nonprofits and the lack of care for the people who benefit from them is perhaps the worst indicator of where we are right now. I'll take some billionaire-directed medical research any day over Peter Thiel calling the giving pledge an “Epstein-adjacent, fake Boomer club.”

Finally, I have to mention the role of the legal industry in this an, as you point out, all the IRS opinion letters that people get to protect themselves from their "playing in the gray." If we did better as tax lawyers, maybe that would help too. I do realize law is a service industry, but saying no to clients who want to do certain things instead of continually thinking of new ways to enable them would be a great start!

(last last thought, I'm curious what you think about split-interest trusts!)

Thanks for the tip on Puerto Rico! Kidding.

How do your children feel about this kind of thinking? Are you leaving them anything?